Understanding the Basics of a Roth IRA Conversion

If you have pre-tax money in a 401k or Traditional IRA and find yourself expecting lower than typical income, consider making good use of lower tax brackets with a Roth IRA conversion.

Sometimes our income from year to year varies.

- People that rely heavily on commissions like real estate agents can have “good” years and “not so good” years.

- Someone who is between jobs or taking a sabbatical could find themselves with very little income in a given year.

- Early retirees, especially those retiring before claiming social security and especially before required 401k and IRA distributions can go from peak earning years to near $0 taxable income all at once.

These fluctuations in our taxable income can create unique planning opportunities to “convert” a portion of our IRA and 401k assets to Roth assets, locking in a low tax rate during low income years and making those converted assets tax-free forever.

Pre-Tax assets vs. Roth assets

First, a quick review of some of the differences between Traditional or pre-tax assets, and Roth assets.

In both cases - the goal is to pay the taxes when you are in the lowest bracket. That means for many people:

- Traditional IRAs are beneficial when you are earning high income putting you in a high tax bracket, and you expect to be in a lower tax bracket when you withdraw the money (i.e. during retirement).

- Roth IRAs are beneficial when you are earning lower income and are in a lower tax bracket (i.e. you are early in your career), and you expect to be in a higher tax bracket when you withdraw the money.

Switching from Pre-Tax to Tax-Free

A conversion allows you to make a deal with the IRS that sounds something like this:

Investor: “I’d like to move this money in my Traditional IRA to a Roth IRA so it can be tax-free so when I take it out”

IRS: “Well, what about the taxes you owe us? We were expecting that revenue you know.”

Investor: “Well, can I just pay the taxes now and be done with it?”

IRS: ::Thinks for a moment:: “Yes, yes just pay us the taxes on the IRA money now, and we will let you put it into the Roth.”

For an investor willing to treat any money you convert from pre-tax to Roth as income in the year you move it, and paying the taxes on it now, the IRS gives you permission to convert your Traditional IRA into a Roth IRA.

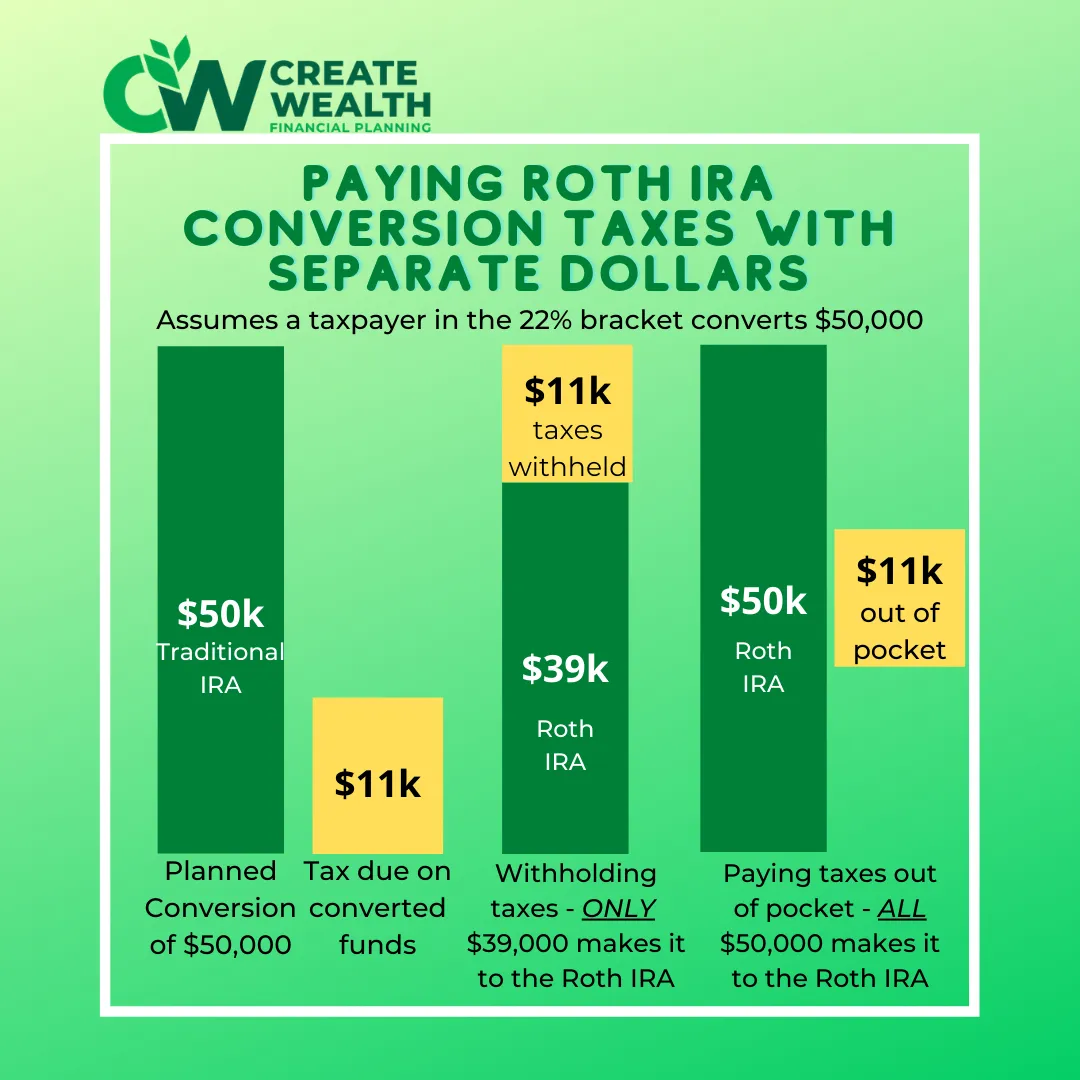

Paying the taxes

When you are presented with the option for a Roth IRA conversion you’ll have the option to pay the taxes “out of pocket” from your cash reserve or other non-retirement funds, or to have money withheld from the amount converted and automatically sent to the IRS. It is typically most effective to pay the taxes from a conversion out of pocket. Otherwise, if you withhold taxes from the amount converted you wind up with less money going into the Roth IRA, cancelling out some of the benefit of the conversion.

Do I have to convert the whole account?

I get this question a lot. You do not have to convert the whole account at once, and in fact the ability to convert small amounts of your pre-tax funds over time can create huge value in the long run. Converting a sizable amount all at once can push you up into higher and higher tax brackets, eliminating all benefits. A very costly mistake indeed. However, there are many situations where a taxpayer may have the ability to spread a large Roth IRA conversion over several years, something we will dive deeper into in a later post.

First steps to considering an IRA conversion

Whether to consider a conversion or not is very situational, and is absolutely something that should be discussed with your financial planner or tax advisor. The last quarter of the year is a popular time to be considering a conversion as most taxpayers will have a pretty good idea of their income situation for the year by October. Large market declines can make other times of the year appealing as well. Conversions must be completed by December 31st of a calendar year to count for that tax year.

If you are anticipating a major change to your taxable income, that’s usually a sign to meet with a trusted professional and see what adjustments should be made. And if it is a significant decline in income, a Roth IRA conversion could be one of those adjustments worth talking about.

You may also like

Home Energy Tax Credits to be Aware of for Major Home Upgrades

What To Do About Your Capital Gains - Part 2