Could Tax Loss Harvesting Enhance your Investment Strategy?

- Sudden drops in the stock market can leave you with negative returns

- Volatile markets can present opportunities for tax-loss harvesting - selling stocks at a loss to allow you to claim the loss for tax purposes

- Read on to learn more about tax-loss harvesting and some rules to be aware of before engaging in tax-loss harvesting transactions

The 2022 investing year has started off with volatility.

Take the S&P 500 – the index of the 500 largest US companies by market value. It opened the year on January 3rd, 2022 at a value of 4778.14, dropped about 9% in January before recovering about half way back. Then it dropped further to about -12% in March before clawing its way back to being down around 7% as of mid-April. This kind of volatility is when a portfolio strategy called tax-loss harvesting can add value to an otherwise declining portfolio. Research has shown that periods of high volatility and relatively low returns, combined with a high marginal tax rate for the investor, create the best environment for tax-loss harvesting1.

With tax-loss harvesting investments are sold at a loss for tax purposes and repurchased at a later date to bring the portfolio back in line. In the meantime, the loss realized from selling the investment can either offset gains found in other parts of the portfolio, or it can offset an investors regular taxable income, up to the IRS limit of $3,000 per year.

Let’s review some of the finer points of tax-loss harvesting.

It only works in Taxable investment accounts

Remember that in a taxable brokerage account, we must file with our taxes each year our gains and losses from the sale of investments as well as dividends and interest. Retirement accounts on the other hand, such as Traditional and Roth IRAs or your 401k, do not report annual gains and losses so there are no losses to take.

The higher your tax bracket, the more value tax-loss harvesting will provide

Your tax losses have the opportunity to offset long-term capital gains which are taxed at 15% for most people as well as short-term taxable gains and regular income (up to the $3,000 limit) which can range from a tax rate of 10% – 37% in 2022. The higher your tax rate, the more valuable it is to take a tax loss. Additionally, some individuals have income low enough that their long term capital gains rate is 0%.2 In this case, offsetting these gains with a tax loss will have zero effect, and in fact for these clients we sometimes try to harvest gains to be able to take advantage of the 0% capital gains rate.

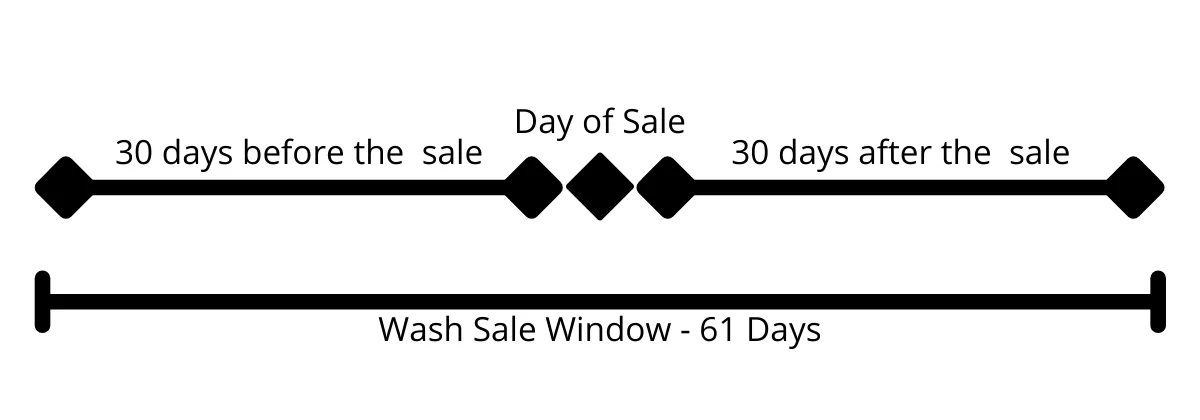

Beware of the wash sale rule

The “wash sale” rule was created by the IRS to discourage investors from selling something at a loss for tax purposes and immediately buying it back. The wash sale rule basically disallows a tax loss when the same or a “substantially identical” investment is bought in the 61-day window that is 30 days before and 30 days after selling an investment for a loss.3 There is no standard definition of “substantially identical” investment4, and buying the investments in other accounts like an IRA or a spouse’s account count too. The issue is that if the money just sits in cash the funds are out of the market for 30 days while you wait for the wash sale time to expire. An experienced investment manager or tax professional may be able to help you reposition the cash during the wash sale window without violating the “substantially identical” rules. Tread lightly here.

Know if transaction costs are a consideration

The good news is that there are so many companies where stocks and exchange traded funds can be bought and sold commission free. That’s not a license to day trade your account, but it’s a nice feature when you or your investment manager wants to reallocate things and keep costs low. If, however, you will incur trading commissions or other transaction costs such as a mutual fund early redemption fee, keep in mind how this could eat away from the tax benefit of your loss-harvesting transaction.

Who knows if the current volatility will continue and for how long? If markets continue to bounce between new highs and steep lows, it could present additional opportunities for you to add value to your portfolio through tax-loss harvesting.

If monitoring your portfolio on a day-to-day basis isn’t for you and you’d like some help with tax-loss harvesting and other investment strategies, reach out to schedule a free call to learn more about working with Create Wealth Financial Planning.

You may also like

What Tax Documents Do I Need For Filing My Tax Return?