How Your Bond Portfolio is Impacted by Interest Rate Changes

Interest rates have been making headlines again. With the Federal Reserve adjusting rates, many investors are asking the same question: What does this mean for the bonds in my portfolio?

In this post, we’ll walk through how bonds react to interest rate changes, what this means for your investments, and why understanding these dynamics is key to building a balanced portfolio.

Why Bonds Still Matter in Every Portfolio

No matter how aggressive or conservative of an investor you are, chances are you hold at least some bonds. Bonds serve as the stabilizing force in a portfolio, offering income and diversification when stocks experience volatility.

But bonds don’t operate in isolation. They’re closely tied to interest rates, and the past several years have been a perfect case study of just how much that connection matters.

We’ve gone from a zero-interest-rate environment after the Great Recession, which brought on a massive housing boom, to one of the fastest rate hikes in decades in 2022. That period even produced the single worst return year for bonds in 50 years. Fast forward to September 2025, when the Fed just cut rates by a quarter of a point. Every shift like this ripples through the bond market.

Two Ways Bonds Produce Returns

To understand the effect of interest rate changes, it helps to know how bonds create value in the first place. There are two main elements:

- Interest Yield (Coupon Payments) When you purchase a bond, you’re essentially lending money to a government, company, or municipality. In exchange, you earn interest, often paid twice a year. The rate you earn is called the coupon rate, and it’s locked in when the bond is issued. Lower interest rates today mean newly issued bonds will pay less in interest compared to older bonds. That’s disappointing for income seekers shopping for new bonds, but it creates opportuinties for existing bondholders.

- Bond Price (Market Value) The second piece is the value of the bond itself. If you already own bonds that pay higher interest than what’s currently available, your bonds become more attractive in the secondary market. Investors must pay a premium to receive those higher interest payments. On the other hand, if interest rates rise and new bonds offer higher yields, your existing bonds may lose some value.

Think of it like a seesaw: when interest rates go down, existing bond values go up. When rates go up, bond values come down.

A Simple Example

Imagine you purchased a U.S. Treasury bond paying 4.5%. A year later, new Treasuries are being issued at only 4%. Your bond is more valuable because it pays more in interest payments than the newly issued bonds of the same type. If you chose to sell it, you could likely do so at a premium.

But flip the scenario: if new Treasuries are paying 5% while you hold that 4.5% bond, buyers will discount your bond, since they can get higher payments elsewhere. That’s how 2022 played out, when rising rates caused many bond values to tumble.

The silver lining is that rising rates benefit new buyers. If you’re looking to add bonds to your portfolio or hold them for income, higher yields mean better payouts. Even savers with money in high-yield savings accounts saw this effect as banks raised interest rates alongside the Fed’s moves a couple of years ago.

Beyond Rates: Other Factors that Influence Bonds

Of course, interest rates aren’t the whole story. Other details also affect bond values, including:

- Credit quality – Government bonds are generally safer than corporate bonds, and companies with lower credit ratings have to pay higher interest to make up for the risk.

- Time to maturity – Longer-term bonds usually carry more risk and pay higher interest, while short-term bonds offer less yield but also less volatility.

- Tax treatment – Municipal bonds, for instance, may come with tax advantages depending on where you live, which can lower the payout.

Still, no matter the type of bond, the relationship between interest rates and bond values remains consistent.

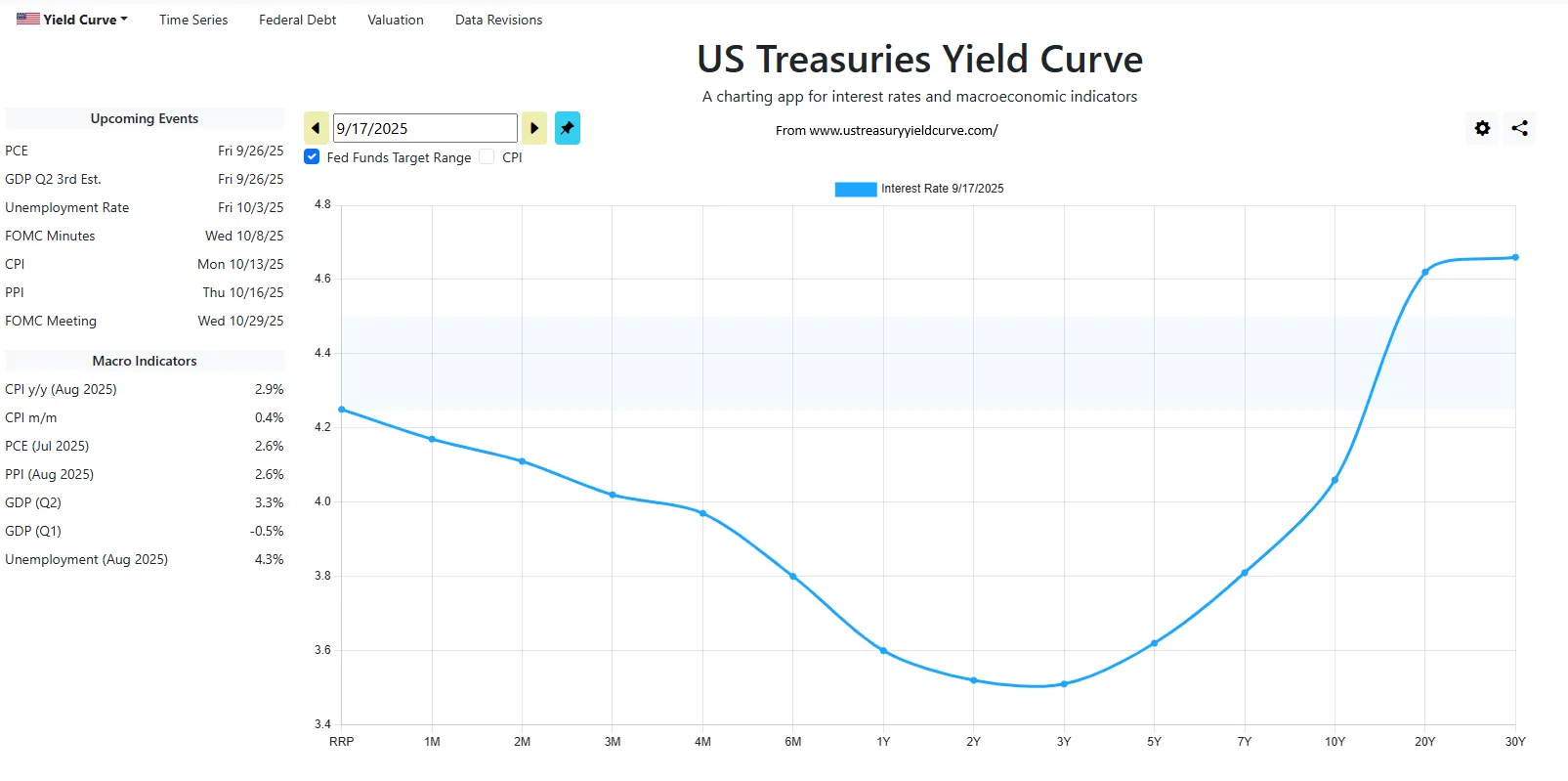

What the Yield Curve Tells Us

Another important tool for understanding bonds is the yield curve. This chart, taken from on 9/18/2025 from www.ustreasuryyieldcurve.com, shows the interest rate on US treasury bonds of different maturities from overnight rates to 30-year treasuries.

In a “normal” yield curve, longer-term bonds pay higher yields. But today, we’re seeing a partially inverted yield curve. That means short-term bonds are offering higher yields than intermediate ones. Only when you stretch out to 10-, 20-, or 30-year maturities do rates climb back up again.

Why does this matter? An inverted curve often signals market expectations that rates may come down in the future. But yield curves aren’t always smooth, and they don’t always move uniformly. Short-term bonds may see gains when rates drop, while intermediate bonds already at lower rates may see less activity, and long-term bonds may shift down but stay above the intermediate bond levels.

Why Diversification Across Bonds Matters

If your portfolio is well-structured, you likely hold bonds of different types, maturities, and risk levels. That’s intentional. Diversification ensures you’re not overly exposed to just one segment of the yield curve.

As interest rates change, some of your bonds may lose value while others gain. Over time, this mix helps smooth out returns and gives you more consistent performance.

The Big Picture: Portfolio Balance

At the end of the day, the most important decision isn’t about guessing where interest rates will go next. It’s about the overall balance between stocks and bonds in your portfolio.

- Stocks drive long-term growth but come with volatility.

- Bonds provide income and stability but are sensitive to rate changes.

Your allocation between the two should reflect your goals, time horizon, and tolerance for risk—not just short-term market moves.

Practical Takeaways

- Don’t overreact to headlines. Interest rates will continue to move up and down. What matters is how your overall portfolio is positioned.

- Understand the seesaw. When rates fall, existing bonds become more valuable; when rates rise, new bonds become more attractive.

- Diversify your bond holdings. Spread across different maturities and credit qualities so you’re not tied to one segment of the market.

- Match your portfolio to your plan. The right mix of stocks and bonds depends on your financial goals, not just today’s interest rate news.

Final Thoughts

Interest rate changes are a fact of investing life, and bonds will always respond. Sometimes that means a boost in value for what you already own. Other times it means an opportunity to buy new bonds at higher yields.

The key is to step back and look at the big picture. A well-balanced portfolio, properly aligned to your personal financial plan, will weather interest rate shifts over time.

If you’re unsure about how bonds fit into your own strategy, or if you’d like to review your portfolio in light of recent interest rate moves, feel free to reach out. I’d be happy to walk you through your options.

Thanks for reading—and as always, stay focused on your long-term goals.

You may also like

Do you invest like a gambler, or are you the house?

Investing 101: Mutual Funds vs. Exchange-Traded Funds (ETFs)