The Power of the HSA: How a Triple-Tax-Advantaged Account Can Boost Your Long-Term Wealth

Health Savings Accounts, or HSAs, often fly under the radar when people think about building long-term wealth. Yet among financial planners, they are often viewed as one of the most efficient tools available when used with an eye toward the long term. HSAs can help you manage health care costs today while creating a valuable reserve for the future. Whether you are focused on reducing taxes, investing for long-term growth, or preparing for the rising costs of healthcare in retirement, an HSA can play a meaningful role in your financial strategy.

What Makes an HSA Unique

A Health Savings Account is a tax-advantaged savings and investment account that can be used only in conjunction with certain types of health insurance, known as high-deductible health plans (HDHPs). What sets HSAs apart is their triple tax advantage, something no other investment account fully offers:

- Tax-deductible contributions – The money you put in may reduce your taxable income.

- Tax-deferred growth – Earnings and interest accumulate without triggering taxes.

- Tax-free withdrawals – When used for qualified medical expenses, your withdrawals are tax-free.

Many accounts, such as Traditional and Roth IRAs can check two of the three boxes, but not all of them. That makes HSAs such a powerful planning tool.

HSA vs. FSA: Understanding the Difference

HSAs are sometimes confused with Flexible Spending Accounts (FSAs), which also help cover medical costs. However, the two accounts have some important differences.

The biggest difference is that an HSA is not “use it or lose it.” With an FSA, funds typically expire after the end of the year, with only limited rollover allowed. An HSA, on the other hand, allows you to keep and grow unused funds indefinitely. If you contribute $5,000 this year and do not need to spend any of it, that full amount remains in your account, ready to grow and compound for future years.

This flexibility can transform an HSA from a short-term spending account into a long-term savings vehicle.

Investing Your HSA for Long-Term Growth

Many HSA users miss one of the biggest opportunities: the ability to invest HSA funds. Once your account balance exceeds a small required cash threshold (often between $500 and $2,000), the remaining money can typically be invested in mutual funds or ETFs, similar to an IRA or 401(k).

If your household budget allows, consider paying medical expenses out of pocket and leaving your HSA funds invested. By doing so, you give those dollars more time to grow tax-free. With the right investment mix and time horizon, your HSA could become a powerful companion to your retirement portfolio, creating a pool of money specifically for future health care costs.

Keep in mind that investing involves risk. Your investment choices should align with your time horizon and comfort level. A financial professional can help you build a suitable strategy.

Eligibility and High Deductible Health Plans

To contribute to an HSA, you must be enrolled in a high-deductible health plan (HDHP) as defined by the IRS. These limits change from year to year, but for 2026:

- Individual Plans must have a minimum deductible of $1,700 and a maximum out-of-pocket max of $8,500.

- Family coverage must have a minimum deductible of $3,400 and a maximum out-of-pocket max of $17,000.

These plans often have lower monthly premiums than traditional health insurance, which can save you money over time. However, they also come with higher deductibles and more potential out-of-pocket expenses. Choosing the right plan involves balancing your expected medical costs, cash flow, and risk tolerance.

Many employers that offer HDHPs also contribute to employees’ HSAs, similar to a 401(k) match. Even a modest contribution from your employer can help offset higher deductibles and accelerate your savings growth.

Withdrawal Rules and Penalties

HSAs are most effective when used for qualified medical expenses, which include costs such as doctor visits, prescriptions, dental care, and vision expenses. If you withdraw funds for non-qualified expenses before age 65, the withdrawal is subject to income tax plus a 20 percent penalty.

After you reach age 65, you can use HSA funds for any purpose without a penalty. Withdrawals used for non-medical expenses after that age are simply taxed as ordinary income, similar to a traditional IRA distribution. This means your HSA can function as a supplemental retirement account once you reach that age.

Beneficiaries and Estate Considerations

HSAs have limited options for beneficiaries. If you name your spouse, they can inherit the account and continue to use it for their own qualified medical expenses tax-free. However, if the account passes to anyone other than a spouse, the entire balance becomes taxable to the beneficiary in the year of your death.

For that reason, HSAs are not ideal tools for generational wealth transfer. They are better viewed as personal health funding vehicles rather than long-term estate assets.

The Uncertain Future of Health Care Costs

Health care costs have risen steadily for decades, and no one can predict exactly how they will evolve. Advances in technology and the growing influence of artificial intelligence could make health care more efficient, or it could become more expensive as the population ages.

Regardless of what the future holds, having dedicated funds set aside for medical expenses is a wise move. Even if your HSA balance grows beyond what you need for health care, you still have the flexibility to use the money for other purposes in retirement.

Putting It All Together

Health Savings Accounts offer a combination of tax benefits, investment opportunities, and flexibility that few other accounts can match. They can serve as both a short-term safety net for medical costs and a long-term investment vehicle for retirement planning.

Before opening or contributing to an HSA, take the time to compare your health insurance options, estimate your annual medical costs, and review your cash flow. For many households with stable income and moderate health care needs, the HSA can be an incredibly effective addition to a financial plan.

If you are unsure whether an HSA makes sense for your situation, or you would like to review your current plan, reach out to Create Wealth Financial Planning for a personalized analysis.

Key Takeaways

- HSAs are the only triple tax-advantaged account, offering tax-deductible contributions, tax-deferred growth, and tax-free withdrawals for qualified expenses.

- Funds in an HSA roll over year to year, allowing long-term accumulation and investment potential.

- HSAs can be invested for future growth, much like retirement accounts, once minimum cash thresholds are met.

- To qualify, you must be enrolled in a high-deductible health plan.

- Withdrawals before age 65 that are not used for medical expenses incur a 20 percent penalty plus income tax.

- After age 65, HSA funds can be used for any purpose without penalty, though non-medical withdrawals are taxed as income.

- HSAs are best for individuals and families who can manage higher deductibles and want to build long-term, tax-efficient savings for health care.

You may also like

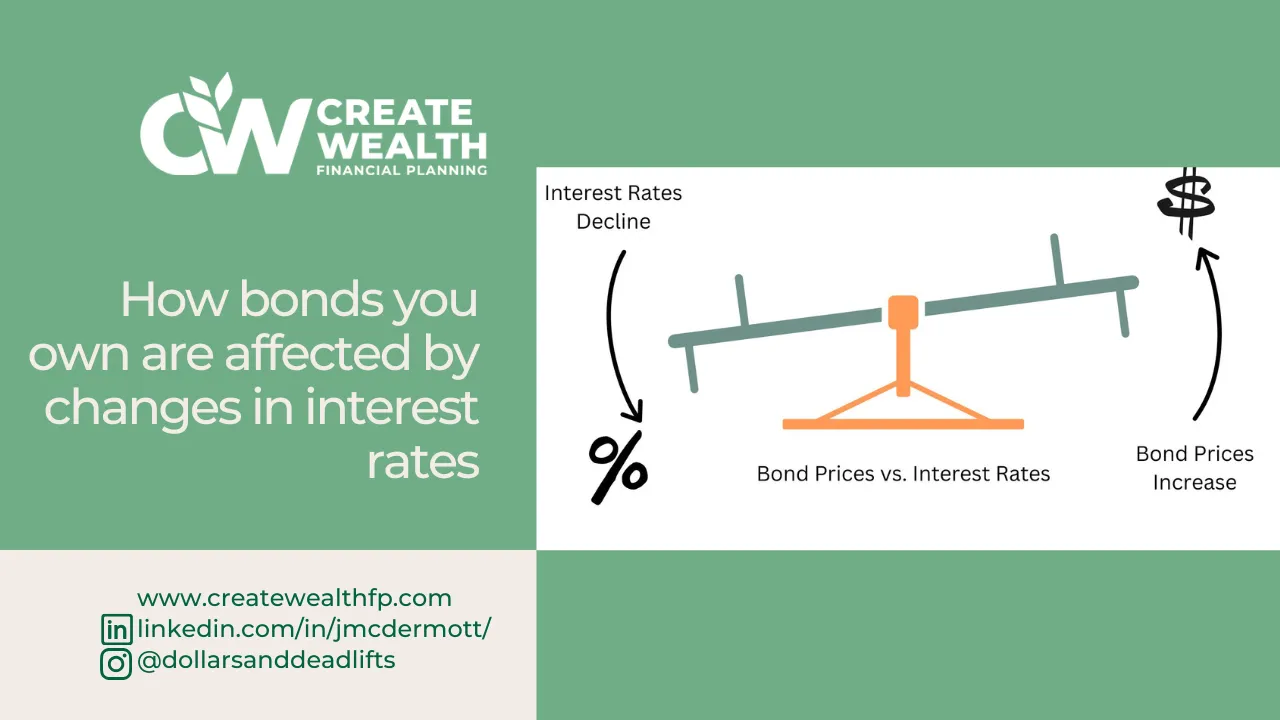

How Your Bond Portfolio is Impacted by Interest Rate Changes

Life Insurance 101 Understanding the Basics